The Cost of Missing a COI Renewal: Real-World Case Studies

The Fort Collins Renovation That Almost Wasn't Covered

Michael thought he had everything under control. The $900,000 retail renovation in Fort Collins was progressing smoothly. His builder's risk policy was set to expire June 30-plenty of time before the projected completion date.

Then a June hailstorm hit. Unexpected damage pushed the finish date to mid-August.

Michael caught the insurance expiration just in time and secured an extension. Two weeks before the revised completion date, thieves broke in overnight and stole $24,000 worth of copper wire and tools.

"If we'd missed that extension deadline, we would have eaten the entire loss," Michael recalls. "Twenty-four thousand dollars out of pocket because of an expired insurance certificate."

Michael was lucky. He caught the expiration before disaster struck. Many contractors and project managers aren't as fortunate.

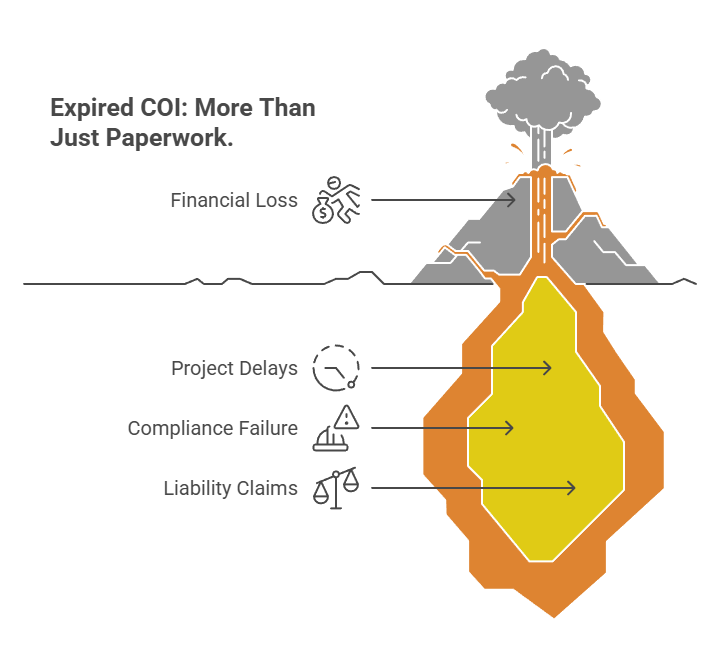

COI mistakes cost contractors $25,000 or more annually. But those aggregated losses hide the real story-the individual incidents where a single expired certificate triggers five-figure costs, project shutdowns, and even six-figure liability claims.

Let's look at what actually happens when COI renewals slip through the cracks.

What Actually Happens When a COI Expires

An expired Certificate of Insurance isn't just an administrative oversight. It's a compliance failure with immediate, measurable consequences.

Immediate Project Impacts

The moment a COI expires, the affected vendor or subcontractor should be removed from the project site. Best practice dictates that construction managers never allow uninsured subs to remain on-site.

This means work stoppage. Equipment sits idle. Crews wait. Project timelines slip. And the clock is ticking on daily carrying costs that don't pause for paperwork problems.

project delays from certificate mistakes average $3,500 per day. For a three-day delay while waiting for updated documentation, that's over $10,000 in direct costs—before accounting for schedule compression expenses to make up lost time.

The Liability Transfer Problem

Here's what many people don't realize about expired COIs: when a third party's insurance lapses, the hiring party becomes responsible for any losses.

If a subcontractor's workers' compensation coverage has expired and someone gets injured, you're not dealing with their insurance company. You're potentially paying the claim directly.

can easily exceed $500,000, especially when property damage or personal injury is involved. The average cost of a construction claim involving uninsured subcontractors ranges from $75,000 to $150,000.

Contractual Consequences

Most construction contracts include specific insurance requirements and maintenance clauses. Allowing work to continue with expired coverage violates those contracts.

This violation can trigger default clauses, expose your organization to breach of contract claims, affect your standing with project owners and general contractors, and create problems for future project bids and bonding capacity.

Even if no incident occurs, the contract violation itself carries risk. Sophisticated owners conduct periodic insurance audits. Discovery of expired coverage—even historical—can lead to disputes, claims, and damaged relationships.

Case Study 1: The $47,000 Subcontractor Injury

A general contractor hired a subcontractor for a commercial building project. The subcontractor submitted a COI showing general liability coverage, and work began.

What Went Wrong

Three months into the project, a subcontractor's employee was injured on-site. The injury wasn't catastrophic—a fall resulting in a broken arm and shoulder damage—but it required medical treatment and time off work.

During the claim investigation, the general contractor discovered the subcontractor's general liability policy had expired six weeks earlier. The subcontractor had let coverage lapse due to cash flow issues and hadn't notified anyone on the project.

The Financial Breakdown

Without active insurance, the injured worker filed a claim against the general contractor. The total cost breakdown:

represents a relatively minor injury. Had the fall resulted in permanent disability or death, the numbers would have been exponentially higher.

What Could Have Prevented It

The general contractor had collected a COI at project start but hadn't implemented renewal tracking. The subcontractor's policy expired mid-project, and nobody caught it until the injury occurred.

Automated expiration tracking with 60, 30, and 15-day renewal alerts would have flagged the upcoming expiration. The contractor could have verified renewal or removed the uninsured subcontractor before the incident occurred.

Case Study 2: The Three-Day Project Shutdown

A drywall subcontractor arrived on-site Monday morning ready to start work on a commercial office renovation. The superintendent asked for their current COI before allowing them on-site—a standard safety check he conducted periodically.

The Discovery

The subcontractor's general liability insurance had expired the previous Friday. They'd missed the renewal deadline and were working to get coverage reinstated, but that process would take several days.

, the general contractor refused to let the crew on-site without valid insurance. Work stopped immediately.

The Domino Effect

The drywall delay triggered a cascade of schedule impacts:

Hidden Costs Beyond Delays

The direct delay cost at $3,500 per day totaled $10,500. But the full impact included:

For a three-day delay caused by an expired certificate, the actual cost exceeded $23,000. And this example represents a relatively minor incident—no injuries, no property damage, just a schedule disruption.

Case Study 3: The Connecticut Construction Fraud

A homeowner hired a contractor for an $84,000 residential renovation. The contractor provided what appeared to be legitimate credentials, including license and insurance information.

The Setup

Work began and progressed for several weeks. Then the contractor abruptly walked out on the project, leaving $61,000 in expenses and unfinished work.

The Fallout

When the homeowner tried to file a claim against the contractor's insurance, they discovered the coverage didn't exist. Further investigation revealed the contractor's license had expired ten years earlier.

illustrates the extreme end of COI fraud—completely fabricated credentials. But lesser versions occur regularly: expired policies, insufficient coverage limits, missing required endorsements, and named insured mismatches.

The homeowner eventually recovered some losses through legal action, but the process took years and cost significant legal fees.

Lessons for COI Verification

This case highlights why simply collecting a COI document isn't enough. Effective verification requires:

Manual verification of these details is time-consuming and often skipped. Automated systems can verify coverage in real-time, flagging discrepancies before work begins.

The Real Numbers: Annual Costs of COI Mistakes

Let's quantify what COI tracking failures actually cost construction companies and project managers annually.

Direct Financial Losses

contractors can eliminate $25,000 or more in annual losses by avoiding common COI errors. This figure includes:

These are the predictable, recurring costs—the death by a thousand cuts that comes from poor certificate management.

Insurance Premium Increases

Here's a hidden cost many organizations don't connect to COI management: contractors dealing with frequent COI corrections face insurance premium increases of 15-30% at renewal.

Why? Insurance companies view poor certificate management as a risk indicator. It suggests inadequate vendor screening and potential for uncovered claims. When carriers see patterns of expired certificates or insurance gaps, they price that risk into your premiums.

For a contractor paying $100,000 annually in premiums, a 20% increase means $20,000 in additional costs—year after year.

Administrative Burden

compliance teams can spend 100-200 hours per year chasing vendors for missing or updated COIs.

Calculate that burden at even a modest hourly rate:

That's just for the tracking and follow-up work—before accounting for the value of higher-level work those team members could be doing instead.

Liability Exposure

The numbers cited so far represent predictable, recurring costs. The real financial risk comes from liability exposure when incidents occur with uninsured or underinsured vendors.

average $75,000-$150,000. But serious incidents can reach much higher.

Consider these documented settlement amounts from construction injury cases:

While not all these cases involved expired COIs specifically, they illustrate the financial exposure construction companies face when proper insurance coverage isn't in place.

The Six-Figure Settlements Construction Companies Want to Avoid

Let's be clear about what's at stake. A single expired certificate can trigger six-figure liability.

When an uninsured subcontractor's employee is seriously injured, you're not dealing with a nuisance claim. You're facing potential exposure that can threaten your business.

Consider this scenario: A subcontractor with lapsed workers' compensation coverage has an employee fall from scaffolding. The worker suffers permanent disability. The lawsuit names your company as the general contractor.

Your exposure includes:

These aren't hypothetical numbers. Construction industry data shows that inadequate COI management can cost companies millions when claims materialize.

The frustrating part? This exposure is entirely preventable. Automated tracking systems catch expiring certificates before they lapse, eliminating the coverage gap that creates liability exposure.

Prevention: How Automated Tracking Eliminates These Risks

Every case study we've examined shares a common thread: the COI lapse went unnoticed until it was too late. An automated approach prevents these scenarios from occurring.

Proactive Renewal Reminders

The most important feature of any tracking system is proactive notification. Automated alerts notify both your team and the vendor well before certificates expire—typically 60, 30, and 15 days out.

This advance warning provides time to:

The Fort Collins renovation we discussed? That contractor caught the expiration because he maintained a tracking calendar. With automated reminders, he wouldn't have needed to remember—the system would have alerted him automatically.

Verification Before Work Begins

The three-day shutdown scenario happened because the expired coverage wasn't discovered until the crew arrived on-site. Effective tracking systems flag expiring certificates before vendors arrive.

send automatic renewal requests to vendors 60 days before expiration. If the vendor doesn't respond or can't provide updated coverage, you know weeks in advance—not when they're standing at the gate ready to work.

Centralized Documentation

The Connecticut fraud case illustrates why centralized, accessible documentation matters. When questions arise—during audits, investigations, or disputes—you need instant access to insurance records.

Cloud-based tracking systems maintain complete history: when certificates were collected, who approved them, what renewals occurred, and what follow-up happened. This documentation protects your organization and demonstrates good faith compliance efforts.

Audit-Ready Compliance

Insurance audits are stressful when you're scrambling to compile documentation from spreadsheets, email folders, and file cabinets. With centralized tracking, you can export comprehensive compliance reports in minutes.

that automated tracking improves compliance rates from 40-60% to over 90%. That's the difference between hoping you're covered and knowing you're covered.

Implementation Guide: Protecting Your Organization

Ready to eliminate the risk of expired COI renewals? Here's your step-by-step plan.

1. Conduct a current state audit

Review your last 12 months of projects. How many COI expirations occurred during active work? How many near-misses happened? What did delays or complications cost you? Understanding your risk exposure justifies investment in better systems.

2. Calculate your real costs

Add up direct costs from COI-related issues: delays, expedited processing, disputes, premium increases, and administrative time. Most organizations underestimate these costs until they calculate them systematically. The total usually exceeds $25,000 annually.

3. Define your insurance requirements clearly

Create standardized insurance requirements for different vendor categories. What coverage types do you require? What limits? What endorsements? Clear requirements make verification straightforward and reduce ambiguity.

4. Establish verification workflows

Decide when and how certificates will be collected and verified. Best practice is collection before contract execution and verification before work begins, with renewal tracking throughout the engagement.

5. Implement automated tracking

Choose a platform that fits your needs. If you're managing numerous expiration types beyond just COIs, systems like Expiration Reminder provide flexibility to track any document with a deadline—insurance certificates, licenses, permits, certifications, and equipment inspections—all in one place.

6. Train your team and communicate with vendors

Everyone involved needs to understand the process. Train project managers on verification requirements. Communicate with vendors about submission procedures. Clear expectations prevent confusion and delays.

7. Monitor compliance metrics

Track key indicators: vendor compliance rate, average time to secure updated certificates, number of expired certificates discovered during projects, and cost savings from avoided incidents. These metrics demonstrate ROI and identify areas for improvement.

8. Refine and optimize continuously

Review your process quarterly. What's working well? Where do certificates still slip through? What vendor categories create most problems? Continuous improvement turns a good process into a great one.

Key Takeaways

Financial Impact

- COI mistakes cost contractors $25,000+ annually through direct losses, with individual incidents ranging from $24,000 to over $150,000

- Insurance premiums can increase 15-30% due to poor certificate management

- Project delays from expired certificates average $3,500 per day

- Administrative burden: 100-200 hours annually spent chasing missing or outdated COIs

Real Risks of Expired COIs

- When a subcontractor's insurance lapses, the hiring party becomes liable for losses

- Construction claims involving uninsured subcontractors average $75,000-$150,000

- Serious incidents can result in six-figure settlements, with some documented cases exceeding $2 million

- Expired COIs trigger immediate work stoppages, project delays, and contractual violations

Common Problem Scenarios

- Subcontractor injuries occurring after coverage lapses expose general contractors to full liability

- Mid-project insurance expirations create cascading schedule delays affecting multiple trades

- Fraudulent or fabricated certificates go undetected without proper verification

- Manual tracking systems fail to catch expirations until it's too late

Prevention Through Automation

- Automated tracking improves compliance rates from 40-60% to over 90%

- Proactive renewal reminders (60, 30, and 15 days out) prevent coverage gaps

- Real-time verification catches discrepancies before work begins

- Centralized documentation provides audit-ready compliance records

Bottom LineThe cost of implementing automated COI tracking is minimal compared to the risk of a single uninsured incident. Most organizations underestimate their exposure until they calculate losses systematically.

Frequently Asked Questions

Q: What should we do if we discover a vendor's insurance expired while they were working on our project?

Take immediate action: remove the vendor from the site until coverage is restored, document the gap period precisely, notify your insurance carrier and legal counsel about the exposure, review whether any incidents occurred during the lapsed period, and verify new coverage thoroughly before allowing work to resume. Even if no incident occurred, you may have contractual obligations to report the lapse to project owners or other stakeholders.

Q: Can we be held liable for a subcontractor's actions even when they have valid insurance?

Yes, depending on the circumstances. General contractors can still face liability claims even when subcontractors carry insurance, particularly under premises liability, direct negligence, and vicarious liability theories. However, proper insurance requirements and additional insured endorsements provide significant protection. The real danger comes when you think a subcontractor has coverage but they don't—then you're almost certainly facing liability without any insurance protection between you and the claim.

Q: How often should we verify that certificates of insurance are still valid?

Best practice is continuous monitoring through automated tracking rather than periodic manual checks. Certificates should be collected before work begins, tracked throughout the engagement with renewal alerts 60, 30, and 15 days before expiration, and reverified if any coverage concerns arise. Waiting for annual or quarterly audits leaves too much exposure window. Organizations using automated systems typically maintain 90%+ compliance compared to 40-60% compliance with manual tracking.

Q: What's the difference between collecting a COI and actually verifying coverage?

Collecting a COI means you have a document—but that document might show expired coverage, insufficient limits, missing endorsements, or even fraudulent information. Verification means confirming the policy is currently active, coverage amounts meet your requirements, required endorsements are in place, the named insured matches the entity performing work, and the certificate was issued by a legitimate insurance agency. The Connecticut case study illustrates why collection alone isn't enough—the contractor had provided insurance information, but it was completely fraudulent.

Q: Our company is small and we only work with a handful of subcontractors. Do we really need automated tracking?

The risk isn't proportional to the number of vendors—it's proportional to the potential exposure. A single uninsured incident can cost $75,000-$150,000 or more, regardless of how many total vendors you work with. Even small operations benefit from automated reminders that prevent that one critical expiration from slipping through. If you're managing fewer than 20 vendors with stable relationships, a simple expiration tracking system provides protection at minimal cost. The question isn't about company size—it's about whether you can afford the five or six-figure cost when a certificate lapses unnoticed.

Q: What happens to our insurance premiums if we have claims involving uninsured subcontractors?

Your premiums will likely increase significantly—potentially 15-30% or more depending on claim severity. Insurance carriers view claims involving uninsured parties as evidence of inadequate risk management and vendor screening. This suggests higher likelihood of future claims. Beyond premium increases, you may face non-renewal if the carrier decides you represent too much risk. Multiple incidents involving uninsured subcontractors can make you difficult to insure at any price. This is why preventing coverage lapses through automated tracking actually protects your insurability and keeps premiums stable.