Administrative Services Only (ASO) is a type of self-funded health insurance arrangement in which an employer provides health benefits to employees but outsources the administrative tasks - such as claims processing, customer services, and network management - to a third-party administrator (TPA) or insurance company.

With an ASO plan, the employer assumes the financial risk of paying employee healthcare claims rather than paying fixed premiums to an insurance provider. This model is commonly used by large businesses to control healthcare costs while maintain flexibility in plan design.

Simplify credential management

Tracking employee certifications and licenses doesn't have to be complicated. Expiration Reminder helps you send automated notification and keep your company compliant.

.png?width=2520&height=1800&name=67a0f630d9bbadc84df0deb5_AI_Scanner_1%20(1).png)

Key Facts

- How ASO Works:

- The employer funds employee healthcare claims instead of paying fixed insurance premiums.

- A third-party administrator (TPA) or insurance company handles administrative tasks like claims processing and compliance.

- The employer may purchase stop-loss insurance to limit financial risk from unexpectedly high claims.

- Benefits of ASO Plans:

- Cost Savings: Employers avoid high insurance premiums and only pay for actual healthcare claims.

- Flexibility: Employers can customize healthcare plans based on employee needs.

- Transparency: Direct control over healthcare spending and claims data.

- Potential Tax Benefits: Employers may save on certain taxes compared to fully insured plans.

- Challenges of ASO Plans:

- Financial Risk: Employers bear the cost of all claims, which can be unpredictable.

- Regulatory Compliance: Employers must follow healthcare regulation, including the Employee Retirement Income Security Act (ERISA) and the Affordable Care Act (ACA).

- Administrative Complexity: Requires efficient management and oversight of the TPA.

- Difference Between ASO and Fully Insured Plans:

- ASO Plan: Employer funds claims, with administration outsourced to a TPA.

- Fully Insured Plan: Employer pays fixed premiums to an insurance company, which assumes all financial risk.

1. What is an ASO (Administrative Services Only) Plan?

An ASO plan is a self-funded health insurance arrangement where an employer provides health benefits directly to employees but outsources the administrative tasks to a third-party administrator (TPA) or insurance company. In this setup, the employer is responsible for funding the claims, while the TPA handles functions such as claims processing, customer service, network management, and compliance with regulations. This arrangement allows employers to have more control over healthcare costs while benefiting from the expertise of the TPA to manage the operational aspects of the health plan. ASO plans are often chosen by larger employers who are looking to reduce healthcare costs and maintain flexibility in plan design.

How Does an ASO Plan Work?

- Employer Funds the Plan

In an ASO plan, the employer takes on the responsibility of funding the health plan directly rather than paying premiums to an insurance company. The employer sets aside a predetermined amount of money to cover the cost of employee healthcare claims, which can include doctor visits, prescription medications, hospital stays, and other medical expenses. This self-funded model allows the employer to have greater control over the funds and potentially save money by only paying for actual claims, rather than fixed premiums.

- Third-Party Administrator (TPA) Manages Claims

To streamline the administrative side of the plan, the employer contracts with a third-party administrator (TPA) or insurance company to handle the day-to-day operations of the health plan. The TPA is responsible for managing and processing claims, ensuring that claims are paid according to the terms of the health plan, and addressing any disputes that may arise. Additionally, the TPA manages billing and coordinates benefits, making it easier for the employer to offer comprehensive health coverage without needing to build an in-house administrative system. The TPA also ensures that the plan complies with various regulatory requirements, such as those set forth by the Affordable Care Act (ACA).

- Stop-Loss Insurance Protects Against High Costs

While ASO plans can offer cost savings and flexibility, they also expose employers to the risk of unexpectedly high healthcare costs. Major surgeries, chronic illnesses, or catastrophic events can result in very high medical claims. To mitigate this financial risk, many employers purchase stop-loss insurance, which acts as a safety net. Stop-loss insurance provides protection by covering claims that exceed a certain threshold. This means that if an individual claim or total healthcare costs for a group exceed a set amount, the stop-loss insurer steps in to cover the excess, reducing the financial burden on the employer. This type of insurance is especially important for employers who want to maintain budget predictability while still offering comprehensive health benefits to employees.

Key Features of ASO Plans

- Cost Control: Employers only pay for actual claims rather than fixed premiums.

- Customization: Employers can design benefits to meet employees' specific needs.

- Flexibility: Companies can adjust coverage based on employee usage and company finances.

- Risk Management: Stop-loss insurance protects against excessive claims.

- Potential Risks: Employers bear financial responsibility for claims, which can be unpredictable.

- Not Ideal for Small Businesses: Works best for medium to large companies that can handle fluctuating healthcare costs.

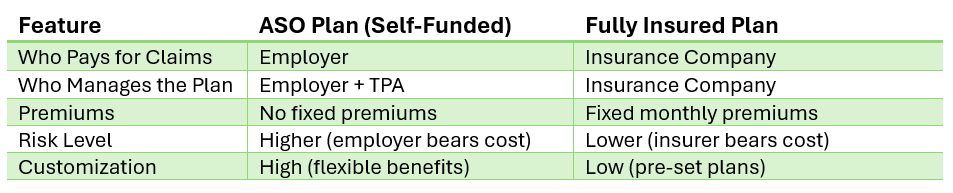

ASO Plan Versus Fully Insured Plan

Who Uses ASO Plans?

- Large and Medium-Sized Businesses: Companies with many employees benefit from lower long-term costs.

- Organizations Seeking Cost Savings: Those wanting more control over healthcare expenses.

- Companies with Healthy Workforce: Lower medical claims reduce the financial risk of a fully insured plan.

Overall, an ASO plan allows employers to fund healthcare benefits directly while outsourcing administrative tasks to a third party, such as a third-party administrator (TPA) or insurance company. This structure offers employers greater control over healthcare costs, providing the opportunity for cost savings, particularly if claims are lower than expected. Additionally, ASO plans offer flexibility, as employers can design a plan that best meets the needs of their workforce, adjusting coverage options and benefits as necessary. However, while ASO plans offer these advantages, they also come with higher financial risk compared to fully insured plans. The employer assumes the responsibility of paying for employee healthcare claims, which can fluctuate due to unexpected medical events or high-cost treatments. To protect themselves against these unpredictable costs, employers often mitigate the financial risk through stop-loss insurance. This safety net ensures that if claims exceed a certain threshold, the stop-loss insurer will cover the excess, providing financial protection for the employer.

Ultimately, an ASO plan strikes a balance between cost control, flexibility, and risk management, making it a popular choice for large employers seeking to optimize their healthcare benefits offering while managing financial exposure.

2. How does an ASO plan differ from a fully insured health plan?

An ASO plan and a fully insured plan are two different ways employers provide healthcare benefits to employees, with the key difference being who bears the financial risk and how claims are funded.

In an ASO plan, the employer assumes the financial risk and funds healthcare claims directly, offering more control over costs but also exposing the employer to potential high expenses. To manage this risk, employers often purchase stop-loss insurance for protection against catastrophic claims. In a fully insured plan, the employer pays a fixed premium to the insurer, which assumes responsibility for funding claims. This limits the employer’s financial liability but offers less flexibility compared to an ASO plan, as customization options are more restricted.

Key Differences Between ASO and Fully Insured Plans

- Financial Risk:

- ASO Plan: The employer assumes the financial risk, funding healthcare claims directly. If claims are higher than expected, the employer bears the costs.

- Fully Insured Plan: The insurance company assumes the financial risk. The employer pays a fixed premium, and the insurer covers healthcare claims, limiting the employer's liability.

- Cost Control:

- ASO Plan: Employers have more control over healthcare costs, as they can adjust benefits and manage claims directly. However, they also face potential financial unpredictability.

- Fully Insured Plan: Employers pay a fixed premium, offering predictable costs but limited ability to control claims and costs.

- Flexibility:

- ASO Plan: Offers greater flexibility in customizing the health plan, including plan design, benefits, and coverage options.

- Fully Insured Plan: Generally offers less flexibility, as the insurance company dictates the plan structure and benefits.

- Claims Management:

- ASO Plan: A third-party administrator (TPA) or insurer manages claims, but the employer is responsible for funding them.

- Fully Insured Plan: The insurer manages and funds claims, making the claims process simpler for the employer.

- Stop-Loss Insurance:

- ASO Plan: Employers often purchase stop-loss insurance to protect against high or unexpected claims, providing a financial safety net.

- Fully Insured Plan: No need for stop-loss insurance, as the insurer takes on the risk of covering high claims.

- Administrative Burden:

- ASO Plan: Requires more administrative oversight from the employer, as they handle claims funding and sometimes work closely with TPAs.

- Fully Insured Plan: Administrative tasks are handled by the insurer, reducing the burden on the employer.

Stop-Loss Insurance for ASO Plans

Stop-loss insurance for ASO plans is a type of insurance purchased by employers to protect themselves from unexpectedly high healthcare costs. In a self-funded ASO plan, the employer assumes the financial risk of paying for employee healthcare claims. However, there is always a chance that claims could exceed expected amounts, especially in the case of major medical events like surgeries, chronic illnesses, or catastrophic injuries.

Stop-loss insurance provides a safety net by covering claims that exceed a certain threshold, known as the "attachment point." This threshold is set by the employer when purchasing the stop-loss policy. For example, if a claim exceeds the attachment point, the stop-loss insurer will pay for the excess costs. This helps limit the employer's financial exposure to unusually high medical expenses, ensuring that the employer's overall healthcare spending remains manageable.

There are two types of stop-loss insurance:

- Specific Stop-Loss Insurance: This covers individual claims that exceed a specified amount. For example, if an employee’s medical expenses surpass the attachment point, the stop-loss insurance kicks in to cover the additional costs.

- Aggregate Stop-Loss Insurance: This provides protection if the total claims for all employees exceed a set amount during a specific period, such as a year. If the total healthcare costs for the group exceed the aggregate attachment point, the stop-loss insurer covers the difference.

By purchasing stop-loss insurance, employers can mitigate the financial risk associated with high medical claims while still benefiting from the flexibility and potential cost savings of a self-funded ASO plan.

Ultimately, ASO plans provide employers with greater cost control and flexibility, allowing them to tailor benefits and pay only for actual healthcare claims. However, this approach requires them to assume financial risk, which can be mitigated through stop-loss insurance. In contrast, fully insured plans offer predictability and lower financial risk, and the insurance company covers all claims. While this provides stability, it comes at a higher costs and limits the employer's ability to customize benefits.

3. What are the advantages of using an ASO plan?

- Cost Savings

One of the main advantages of an ASO (Administrative Services Only) plan is the potential for significant cost savings. Since employers are self-funding the health benefits, they only pay for actual claims rather than a fixed premium to an insurer. This allows employers to save money if claims are lower than expected. Additionally, employers can avoid paying state insurance taxes and insurer administrative fees, which can further reduce costs. - Greater Flexibility and Control

ASO plans offer employers more flexibility and control over their healthcare benefits. Employers can customize the plan design to meet the specific needs of their workforce, such as offering certain health benefits or tailoring coverage options. They also have more freedom in how claims are processed and managed, allowing them to make changes based on employee feedback or cost management goals. - Transparency and Access to Data

With an ASO plan, employers often have direct access to detailed data about claims, utilization patterns, and healthcare costs. This transparency allows employers to make data-driven decisions to improve the plan’s efficiency, optimize healthcare services, and implement cost containment strategies, such as wellness programs or preventive care initiatives. - Potential for Lower Administrative Costs

Employers working with a third-party administrator (TPA) to manage an ASO plan often experience lower administrative costs compared to fully insured plans. TPAs have specialized expertise in claims processing, billing, and compliance management, enabling employers to streamline operations without the need for an internal administrative team. As a result, employers can often achieve more cost-effective plan administration. - No Premium Taxes

Unlike fully insured plans, ASO plans are not subject to state premium taxes. This can lead to savings for employers, particularly in states with high premium tax rates. Eliminating these taxes gives employers more flexibility to allocate funds directly to employee health benefits. - Stop-Loss Insurance Protection

While ASO plans expose employers to the risk of higher-than-expected healthcare claims, they can mitigate this risk by purchasing stop-loss insurance. This coverage protects employers by capping the amount they must pay out-of-pocket for catastrophic or unexpected claims, offering financial security without sacrificing the cost-saving benefits of self-funding. - Better Risk Management

With the ability to analyze claims data and implement targeted health initiatives, employers can engage in better risk management with an ASO plan. By identifying areas where claims may be reduced or health outcomes improved (e.g., preventive care, chronic disease management), employers can take proactive steps to manage healthcare costs over time. - Employee Satisfaction and Retention

ASO plans allow employers to offer customized health benefits that may better align with their workforce's needs. By designing a plan that appeals to employees—whether through enhanced coverage options, wellness incentives, or additional health resources—employers may increase employee satisfaction and improve retention rates. - Increased Control Over Plan Design

Employers have more influence over the specific benefits and coverage options they offer through an ASO plan. This flexibility enables them to include unique services, such as telemedicine, mental health support, or wellness programs, that can improve employee health and engagement, while fully insured plans may have limitations on what they can offer. - Potential for Financial Stability

For larger employers, an ASO plan may provide more predictability and control over healthcare expenses compared to traditional insurance premiums. By managing claims directly and investing in preventative care, employers can create a more sustainable, long-term healthcare strategy that helps stabilize future costs.

In summary, an ASO plan offers employers a variety of advantages, including potential cost savings, increased flexibility, better control over plan design, and enhanced data transparency. However, these benefits come with the responsibility of managing the financial risk associated with self-funding, which is why stop-loss insurance is often purchased to reduce exposure to high claims.

4. What risks do employers face with an ASO plan?

- Financial Risk of High Claims

One of the biggest risks employers face with an ASO plan is the financial responsibility for high or unexpected healthcare claims. Since the employer is self-funding the health benefits, they must cover the cost of employee medical expenses directly. If there are large claims, such as major surgeries, chronic illnesses, or catastrophic health events, the employer may face substantial out-of-pocket expenses. While stop-loss insurance can mitigate this risk, it does not eliminate it entirely, and employers may still experience significant financial exposure. - Cash Flow and Liquidity Challenges

Employers must set aside enough funds to cover ongoing medical claims, which can be unpredictable and vary greatly from month to month. This cash flow challenge means that employers need to ensure they have sufficient liquidity to pay claims as they arise. In cases where claims are particularly high or the employer has an unexpectedly high volume of medical claims, there may be a strain on company resources. - Administrative Burden

Even though the employer outsources certain administrative tasks to a third-party administrator (TPA), the responsibility for managing the plan and ensuring compliance with federal regulations (such as ERISA and the Affordable Care Act) ultimately lies with the employer. This can create an administrative burden, especially for smaller businesses without a dedicated HR or benefits team. Employers must stay on top of regulatory requirements, manage the relationship with the TPA, and ensure that the plan runs smoothly, which can require significant time and effort. - Compliance Risks

Employers offering an ASO plan must adhere to complex federal regulations, including those under ERISA and the Affordable Care Act (ACA). Failure to comply with these regulations can result in legal penalties, fines, and lawsuits. Additionally, ASO plans must ensure they meet all reporting and disclosure requirements, such as providing the Summary Plan Description (SPD) and filing the Form 5500 annually. Employers who don't have the expertise to navigate these requirements may risk falling out of compliance. - Risk of Inaccurate Claims Management

The effectiveness of an ASO plan depends on the performance of the third-party administrator (TPA) in managing claims. If the TPA does not process claims accurately or efficiently, it can lead to delays, overpayment, or errors in benefits administration. Employers must carefully vet and monitor the performance of the TPA to ensure that claims are being managed appropriately. Poor claims management could result in dissatisfied employees, increased administrative costs, or even legal action if claims are mishandled. - Potential for Increased Healthcare Costs

While ASO plans can offer cost savings, there is still a risk that healthcare costs could increase unexpectedly. Medical inflation, changes in healthcare utilization patterns, or a higher-than-expected number of employees requiring costly treatments can drive up overall expenses. Employers may struggle to manage these rising costs without being able to rely on the predictability of a fixed premium, which is the case with fully insured plans. - Employee Dissatisfaction Due to Coverage Limitations

Although ASO plans offer greater flexibility, there is still a risk that employees may feel their healthcare needs are not fully met if coverage options are too limited or if there are delays in claims processing. If employees feel their medical expenses are not adequately covered or experience issues with claim reimbursements, it could result in dissatisfaction, decreased morale, and even lower employee retention. To avoid this, employers must carefully design and communicate their health benefits to ensure employees understand the coverage available. - Increased Complexity with Stop-Loss Insurance

While stop-loss insurance helps protect employers from high claims, it can add another layer of complexity to the plan. Employers need to carefully evaluate the terms and coverage limits of the stop-loss policy, which can vary significantly. Incorrectly assessing the necessary coverage could lead to gaps in protection, potentially leaving the employer exposed to more financial risk than expected. - Impact on Employee Recruitment and Retention

While an ASO plan can be designed to offer competitive benefits, if the plan’s coverage is not perceived as comprehensive or if employees experience difficulties with claims or reimbursement, it may impact employee recruitment and retention. Companies that fail to offer robust healthcare coverage or provide a smooth claims experience may find it more difficult to attract and retain top talent, especially in competitive job markets where benefits are a significant consideration.

While ASO plans offer flexibility and cost-saving opportunities, they also come with inherent risks. Employers face financial risks from high claims, administrative burdens, and compliance complexities, as well as potential challenges in managing cash flow, claims, and employee satisfaction. To mitigate these risks, employers often purchase stop-loss insurance, carefully manage their TPA relationships, and stay vigilant about regulatory requirements. However, those considering an ASO plan must weigh these risks against the potential benefits to determine whether it's the right fit for their business and workforce.

5. Which companies benefit most from ASO plans?

ASO plans are particularly advantageous for certain types of companies, especially those that can handle the financial risk and administrative complexity of self-funded health benefits. Companies that stand to benefit the most from ASO plans include the following:

- Large Companies with a High Employee Headcount

- Why they benefit: Large employers with a large employee population often benefit most from ASO plans due to their ability to spread risk across a larger pool of individuals. This helps stabilize healthcare costs and makes it easier to absorb fluctuations in claims. Larger organizations can also better handle the administrative burden and compliance requirements associated with self-funding.

- Example: Corporations with thousands of employees across multiple locations or departments often choose ASO plans for the potential cost savings and customization options they offer.

- Companies with Predictable Healthcare Claims

- Why they benefit: Companies that have predictable and stable healthcare claims, such as those with a healthy workforce or lower-risk employees, can benefit from the cost savings offered by ASO plans. Since these companies are less likely to incur large or catastrophic medical expenses, they can save money by only paying for the actual claims incurred rather than fixed premiums.

- Example: Businesses with employees in industries with lower healthcare utilization, such as technology or finance, may find ASO plans more cost-effective.

- Companies Seeking Greater Control Over Healthcare Plans

- Why they benefit: Employers who want more control over their healthcare plans and benefits will find ASO plans appealing. With ASO, employers have the flexibility to design their own benefits packages, manage claims directly, and customize the plan to meet the specific needs of their workforce. This flexibility is ideal for companies looking to offer tailored benefits or unique wellness programs.

- Example: Companies in industries with diverse employee needs, such as tech firms offering wellness programs or healthcare providers wanting to include specialized coverage, would benefit from the customization available with ASO plans.

- Companies with Strong Financial Resources

- Why they benefit: Self-funding an ASO plan requires an upfront investment in healthcare claims and administrative services. Companies with strong cash flow and financial stability are better suited for taking on this financial risk. While stop-loss insurance can mitigate the risk of high claims, the employer still needs the liquidity to handle month-to-month fluctuations in healthcare expenses.

- Example: Large manufacturing companies or global corporations with a solid financial standing can afford the risks associated with ASO plans and still benefit from the flexibility and potential cost savings.

- Companies with a Health-Conscious Workforce

- Why they benefit: Employers that prioritize employee wellness and have a health-conscious workforce can leverage the flexibility of an ASO plan to promote preventive care, wellness programs, and health initiatives. These types of companies may see lower healthcare costs and fewer claims due to the healthier habits of their employees, making an ASO plan an attractive option for cost management.

- Example: Companies in the wellness, fitness, or healthcare sectors that focus on maintaining a healthy workforce may reduce the risk of large claims through lifestyle programs and preventive care, making ASO plans a good fit.

- Companies Looking for Transparency and Data-Driven Decisions

- Why they benefit: ASO plans offer detailed insights into healthcare usage and claims data, giving employers the transparency to make informed, data-driven decisions. Companies that value these insights and want to use the information to implement cost-saving strategies or improve employee health outcomes can benefit from the reporting and analytics that come with ASO plans.

- Example: Data-driven organizations, such as financial institutions or tech companies, may use this data to adjust their benefits or implement wellness initiatives, optimizing their healthcare spending.

- Companies That Want to Avoid State-Level Insurance Regulations

- Why they benefit: Companies in states with high insurance premiums or strict insurance regulations may find ASO plans advantageous. Since ASO plans are self-funded and governed by federal laws (such as ERISA), employers are exempt from state-specific mandates and insurance taxes, potentially saving money on premiums and administrative fees.

- Example: Businesses in high-premium states like New York or California could use ASO plans to avoid state taxes on insurance premiums and take advantage of more favorable cost structures.

- Companies Willing to Manage the Administrative Burden

- Why they benefit: ASO plans come with more administrative responsibility, as employers must oversee the plan’s funding, claims management, and compliance with regulations. Companies with internal resources or those willing to partner with a third-party administrator (TPA) to handle claims processing and compliance are more likely to benefit from the cost savings and flexibility offered by ASO plans.

- Example: Mid-to-large businesses with dedicated human resources or benefits teams, or those that work closely with a TPA, are better positioned to handle the administrative workload and maximize the advantages of an ASO plan.

- Companies Focused on Long-Term Cost Management

- Why they benefit: For companies that are looking to take a long-term approach to cost management and healthcare planning, ASO plans provide the flexibility to implement sustainable strategies, such as wellness programs or chronic condition management initiatives, that can reduce future healthcare costs.

- Example: Employers in industries where healthcare is a significant expense (e.g., manufacturing, retail, and logistics) may adopt ASO plans to better manage and reduce their healthcare spending over time.

- Multi-State or Large Regional Employers

- Why they benefit: Employers that operate across multiple states may prefer ASO plans because they allow for consistent, centralized plan management and can help avoid the complications of managing multiple state-mandated plans. ASO plans allow for uniform benefits, policies, and cost management strategies across the workforce, regardless of geographic location.

- Example: National retailers or large service companies with employees spread across several states might prefer the uniformity and simplicity of an ASO plan to ensure consistent health benefits nationwide.

Altogether, large companies, financially stable businesses, and organizations with healthy, engaged workforces are the types of companies that most benefit from ASO plans. These companies can handle the administrative responsibilities and financial risks associated with self-funding while leveraging the flexibility, transparency, and potential for cost savings that ASO plans offer. However, smaller companies or those with limited resources may find the administrative complexity and financial risk of ASO plans more challenging to manage.

Make sure your company is compliant

Say goodbye to outdated spreadsheets and hello to centralized credential management. Avoid fines and late penalties by managing your employee certifications with Expiration Reminder.

.png?width=400&height=300&name=_-%20visual%20selection%20(2).png)